Learn practical strategies to improve cash flow, manage expenses, and build financial stability for your small business in the Philippines.

Running a business in the Philippines is rewarding, but it also comes with financial challenges. Many entrepreneurs struggle not because their products are weak, but because their money flow is not properly managed. This is why understanding small business cash flow Philippines strategies is essential for survival and long term growth.

Cash flow is the movement of money in and out of your business. If more money is going out than coming in, even a profitable business can collapse. In this guide, you will learn practical, Philippines specific techniques to improve your cash flow, avoid common mistakes, and build a financially stable operation.

Table of Contents

Understanding Cash Flow in the Philippine Business Context

Before applying financial strategies, business owners must understand how cash flow works in daily operations within the Philippine market. Local conditions, payment culture, and regulatory requirements directly affect how money moves through a business. Clear understanding builds smarter decisions and long term financial stability.

What Is Cash Flow

Cash flow refers to the movement of money entering and leaving your business within a specific period. It determines whether you can cover expenses, reinvest profits, and sustain operations without financial stress.

Cash flow includes:

- Money coming in from sales, services, or investments

- Money going out for rent, salaries, inventory, utilities, taxes, and loan payments

Positive cash flow means income exceeds expenses, allowing smoother operations and financial flexibility. Negative cash flow happens when expenses are higher than available funds, which can quickly create pressure. Many Filipino entrepreneurs focus mainly on increasing sales, yet strong revenue alone does not guarantee healthy small business cash flow Philippines management.

Why Cash Flow Problems Are Common in the Philippines

Cash flow challenges are common because of specific local realities that affect small enterprises across different industries. Economic conditions, infrastructure limitations, and payment practices can disrupt the steady movement of money.

Common local challenges include:

- Delayed customer payments, especially in business to business transactions

- Seasonal demand fluctuations throughout the year

- Typhoon related operational disruptions

- High electricity and logistics expenses

- VAT and other tax compliance requirements

Businesses must comply with regulations from the Bureau of Internal Revenue, which requires taxes to be paid on time even if customer payments are still pending. This situation places pressure on working capital and requires disciplined financial planning.

Why Cash Flow Management Is Critical for Small Businesses

For many entrepreneurs in the Philippines, cash flow determines whether a business survives or struggles. Small businesses often operate with limited capital, making careful financial management essential for daily operations and long term sustainability.

Healthy cash flow allows businesses to pay suppliers, employees, rent, and utilities without interruption. It also gives owners the flexibility to invest in growth opportunities such as expanding inventory, improving marketing, or upgrading equipment.

Poor cash flow management can quickly create operational pressure even if the business is profitable on paper. When funds are not available at the right time, businesses may face delayed payments, supplier issues, or difficulty covering essential expenses.

Strong cash flow management helps small businesses:

- Maintain consistent operations

- Handle unexpected expenses

- Build financial stability

- Plan for future growth

By understanding how money moves through the business and applying disciplined financial practices, entrepreneurs can create a more stable foundation for long term success in the Philippine market.

8 Tips to Improve Small Business Cash Flow in the Philippines

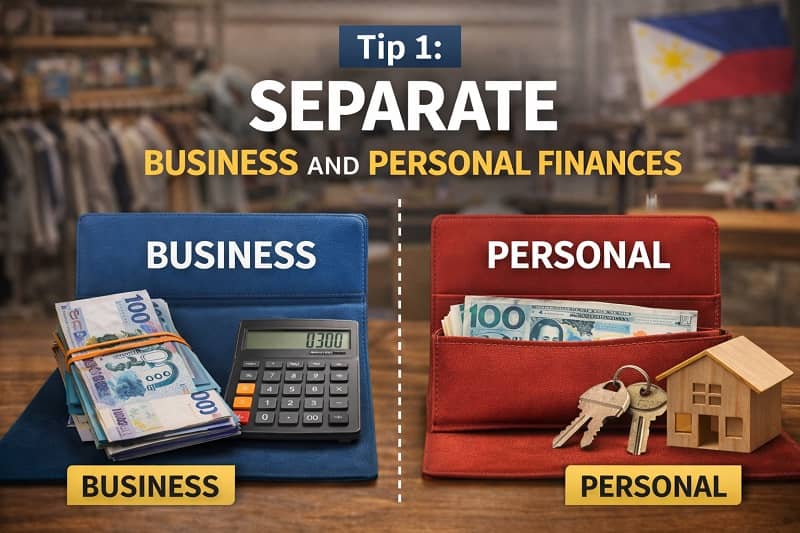

Tip 1: Separate Business and Personal Finances

Many small businesses in the Philippines begin as family managed ventures. Although this setup is common, combining personal and business funds often causes confusion, inaccurate records, and unexpected shortages. Clear financial boundaries help owners monitor performance properly and protect overall small business cash flow Philippines stability.

Open a Dedicated Business Bank Account

Even if you operate as a sole proprietor registered with the Department of Trade and Industry, maintaining a dedicated business account is essential for proper financial management. Separation builds discipline and improves transparency in daily transactions.

You should:

- Open a separate business account

- Track income and expenses clearly

- Avoid withdrawing business funds for personal spending

Taking this simple step strengthens financial control, improves reporting accuracy, and makes small business cash flow Philippines management more organized and reliable over time.

Tip 2: Forecast Your Cash Flow Monthly

Forecasting cash flow each month allows business owners to anticipate possible shortages before they become serious problems. By reviewing expected income and expenses in advance, you gain better control over spending decisions and protect small business cash flow Philippines stability throughout the year.

Create a Simple Cash Flow Projection

A cash flow projection outlines the money you expect to receive and the payments you must make within a specific month. This planning tool helps you identify gaps early and prepare appropriate adjustments.

List:

- Expected income for the month

- Fixed expenses such as rent, salaries, and internet

- Variable expenses such as inventory and utilities

- Tax obligations

You can create this projection using a basic spreadsheet or accounting software. Consistent monitoring prevents financial surprises and reduces unnecessary stress.

Prepare for Seasonal Fluctuations

Seasonal patterns strongly influence revenue in many Philippine industries. Recognizing these trends allows you to adjust spending and save during high earning months.

For example:

- Retail businesses earn more during Christmas season

- Agricultural businesses depend on harvest cycles

- Tourism businesses slow down during typhoon months

Planning ahead for slower periods supports steady small business cash flow Philippines performance and helps maintain operational stability year round.

Tip 3: Improve Your Collections Process

Late payments are one of the most common causes of cash flow problems for small businesses in the Philippines. When receivables are delayed, operations suffer and financial planning becomes difficult. Strengthening your collections process protects small business cash flow Philippines consistency and supports smoother daily operations.

Set Clear Payment Terms

If you extend credit to customers, establish clear and professional payment terms from the beginning. Defined expectations reduce misunderstandings and encourage timely settlement of obligations.

If you offer credit:

- Define payment deadlines clearly

- Add small penalties for late payments

- Send reminders before due dates

Service based businesses may also request partial upfront payments. This approach lowers financial risk and improves short term liquidity.

Offer Digital Payment Options

Digital payment systems make transactions more convenient and efficient for both businesses and customers. Faster payment methods reduce processing time and improve cash availability.

Consider offering:

- GCash

- Maya

- Online bank transfers

Compared to manual collection methods, digital options reduce delays and strengthen small business cash flow Philippines stability through quicker access to funds.

Tip 4: Control Inventory Wisely

Inventory management directly affects your available cash. Excess stock ties up money that could support other expenses, while insufficient stock results in missed sales opportunities. Maintaining the right balance helps preserve liquidity and strengthens small business cash flow Philippines performance across different seasons.

Apply Basic Inventory Management

Effective inventory control requires consistent monitoring and disciplined purchasing decisions. Understanding which products sell quickly and which move slowly prevents unnecessary capital from being locked in storage.

You should:

- Track fast moving products

- Avoid overstocking slow items

- Negotiate better supplier payment terms

Using simple technology tools such as POS systems allows real time tracking of inventory movement. Accurate data supports smarter purchasing decisions and improves overall cash flow control.

Tip 5: Manage Operating Expenses Carefully

Managing operating expenses is essential for protecting business stability. Reducing unnecessary costs immediately improves liquidity and strengthens financial control. Careful spending decisions allow owners to allocate funds more effectively and maintain healthy small business cash flow Philippines performance throughout different economic conditions.

Review Monthly Fixed Costs

Regularly reviewing fixed expenses helps identify areas where savings are possible without affecting service quality. Even small adjustments can produce meaningful improvements in overall financial performance.

Ask yourself:

- Can you renegotiate your rent?

- Can you shift to a cheaper supplier?

- Can you reduce electricity usage?

In the Philippines, electricity rates are among the highest in Southeast Asia. Improving energy efficiency and monitoring consumption can create noticeable monthly savings.

Avoid Unnecessary Debt

Loans can support business growth, yet they also increase fixed monthly obligations. Borrowing without careful evaluation may create additional pressure on cash flow.

Only borrow when:

- The return on investment is clear

- Cash flow projections show ability to pay

Always compare interest rates, repayment terms, and total costs before making a final decision. Careful borrowing protects long term financial stability.

Tip 6: Build an Emergency Cash Reserve

Unexpected events such as typhoons, supplier delays, equipment breakdowns, or sudden repairs can interrupt normal operations and reduce revenue. Without a financial buffer, these disruptions may quickly strain daily expenses and payroll. Preparing ahead protects small business cash flow Philippines stability during uncertain periods.

Aim to build a reserve equal to at least three months of operating expenses. This safety fund allows your business to continue paying rent, salaries, and utilities even when income slows. A solid buffer strengthens confidence and supports steady decision making during financial pressure.

Start small if necessary and build consistently over time. Setting aside a fixed percentage of monthly profit creates a disciplined saving habit. Gradually increasing your reserve improves resilience and ensures your business can recover more smoothly from temporary setbacks or emergencies.

Tip 7: Monitor Tax Obligations and Compliance

Taxes have a direct impact on business cash flow because payments must be made on schedule regardless of income timing. Missing deadlines can lead to penalties and interest charges that increase expenses. Careful tax monitoring protects small business cash flow Philippines stability and prevents avoidable financial strain.

Always practice disciplined tax management:

- Set aside tax portions from every sale

- Track VAT obligations if applicable

- File returns on time

Separating tax funds from operating cash reduces the risk of accidental spending and helps maintain accurate financial records.

For official guidelines and updated regulations, visit the Bureau of Internal Revenue website at https://www.bir.gov.ph to confirm requirements based on your business classification. Staying informed supports compliance and reduces uncertainty.

Tip 8: Use Technology to Improve Financial Visibility

Digital tools are transforming how small businesses manage finances in the Philippines. Government and private sector initiatives continue to promote digital adoption among SMEs. Even simple systems can improve accuracy, reduce manual errors, and strengthen small business cash flow Philippines oversight and decision making.

Use Accounting Software

Accounting software helps business owners track transactions and generate reliable financial reports without complex manual processes. Organized data improves transparency and supports more confident financial planning.

Benefits include:

- Automatic expense tracking

- Real time financial reports

- Easier tax preparation

- Better forecasting

Cloud based platforms allow owners to monitor finances from any location with internet access. Access to updated financial data enables faster decisions and improves long term cash flow management.

Common Cash Flow Mistakes to Avoid

Cash flow problems often arise from preventable mistakes rather than lack of effort. Even experienced entrepreneurs can overlook financial details that gradually weaken stability. Recognizing these common errors helps protect small business cash flow Philippines performance and supports more disciplined financial management.

Common mistakes include:

- Expanding too fast without capital support

- Offering unlimited credit to customers

- Ignoring small daily expenses

- Failing to forecast taxes

- Relying only on profit reports instead of cash flow statements

It is important to understand that profit is not the same as available cash. A business may appear profitable in reports while lacking enough funds to cover immediate expenses and obligations.

Final Thoughts on Small Business Cash Flow in the Philippines

Managing small business cash flow Philippines operations does not require complex financial theories. It requires discipline, careful planning, and consistent monitoring of income and expenses. Business owners who stay organized and proactive are better prepared to handle challenges and maintain steady financial performance.

When you:

- Separate finances

- Forecast monthly

- Control expenses

- Improve collections

- Prepare for taxes

- Build reserves

You establish a strong financial foundation that supports long term growth and operational stability.

Healthy cash flow provides confidence and flexibility. It enables you to invest in marketing initiatives, hire skilled employees, upgrade technology, and expand services without constant financial pressure. Stable finances allow smarter decisions and reduce unnecessary stress.

In the Philippine business environment, resilience determines sustainability. With proper systems and disciplined financial habits, your small business can move beyond short term survival and achieve steady, long term success.

More Business Resources for Small Business Owners in the Philippines

Building strong financial habits is only one part of growing a successful enterprise. If you want to strengthen your foundation, improve compliance, and make smarter financial decisions, explore these practical guides designed for Filipino entrepreneurs.

- How to Register a Business Name in the Philippines

- Understanding Basic Business Taxes in the Philippines

- Barangay Clearance, Mayor’s Permit, and BIR Explained Simply

- How to Price Your Products or Services as a Filipino Business Owner

- Best Free Software for Small Businesses in the Philippines

Each guide provides clear, step by step explanations tailored to the Philippine business environment. Continue learning, apply what you discover, and take steady action toward building a more stable and profitable business.

FAQs About Small Business Cash Flow in the Philippines

What is cash flow management and why is it important for small businesses in the Philippines?

Cash flow management tracks money coming in and going out. It helps Filipino entrepreneurs pay expenses on time, avoid shortages, and maintain stable business operations consistently.

How can small businesses improve their cash flow quickly?

Businesses can improve cash flow by speeding up collections, reducing unnecessary expenses, negotiating better supplier terms, and closely monitoring daily transactions to prevent financial surprises.

Why do many small businesses experience cash flow problems?

Many small businesses face cash flow problems due to delayed customer payments, high operating costs, poor budgeting, seasonal sales fluctuations, and limited access to affordable financing.

How often should a small business review its cash flow?

Small businesses should review cash flow weekly or monthly, depending on transaction volume. Regular monitoring helps detect shortages early and supports better financial decision making.

Is profit the same as positive cash flow?

Profit and cash flow are different. A business can report profit but still struggle with unpaid receivables, leaving insufficient cash available for immediate expenses.

How can forecasting help manage cash flow effectively?

Forecasting estimates future income and expenses based on trends. It allows business owners to prepare for slow months, tax obligations, and unexpected costs responsibly.

What role do taxes play in cash flow management?

Taxes directly affect cash flow because payments must be made on schedule. Setting aside funds regularly prevents penalties and protects financial stability.

Should small businesses build an emergency fund?

Yes, building an emergency fund provides protection during disruptions like natural disasters or sudden repairs. It ensures operations continue even when revenue temporarily declines.

How can technology improve cash flow management?

Technology such as accounting software and digital payment systems improves tracking accuracy, speeds up collections, and provides real time financial reports for better decisions.

When should a small business consider taking a loan?

A small business should consider a loan when projected returns exceed borrowing costs and cash flow forecasts confirm the ability to meet repayment obligations.

HD Quiz Hub!

Test your knowledge and reinforce practical lessons from the guide.

Results

#1. What does positive cash flow mean?

#2. Why should business and personal funds be separated?

#3. How often should cash flow be reviewed?

#4. What is a common cause of cash flow problems?

#5. Why is forecasting important?

#6. What should businesses set aside regularly?

#7. How can technology help cash flow?

#8. Why build an emergency fund?

#9. What is inventory overstocking risk?

#10. When is taking a loan advisable?

Thank you for taking the quiz.

Share your score or experience in the comments and let us know how you did.